The size thresholds for charities and not-for-profit (NFP) entities registered with the ACNC have been substantially increased. This will result in far fewer entities requiring an audit or review. However, the ACNC has also mandated the adoption of Related Party and Key Management Personnel (KMP) disclosures for medium and large charities.

Size threshold changes

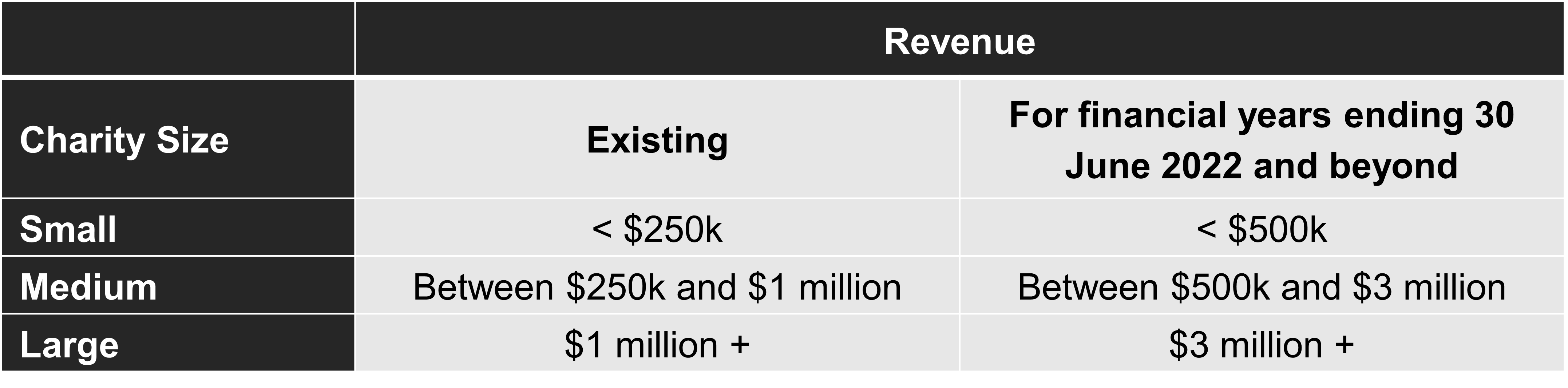

The size thresholds for charities and not-for-profit (NFP) entities registered with the ACNC have been substantially increased. This will result in far fewer entities requiring an audit or review. For financial years ending on 30 June 2022 and beyond, ACNC registered entities will need to record revenue of at least $500k before the requirement for an audit or review of the financial statements kicks in.

Related party disclosures

At the larger end of town, large charities preparing special purpose financial statements and with two or more Key Management Personnel (KMP) will be required to include KMP remuneration disclosures (from AASB 124 Related Party Disclosures).

For financial years ending on 30 June 2023 and beyond, this requirement will also capture medium sized charities and grow to incorporate all disclosures requirements from AASB 124 Related Party Disclosures.

As an alternative to the requirements of AASB 124, charities may choose to apply the disclosures contained in AASB 1060 Tier 2 Simplified Disclosures. There are no substantive differences between the related party disclosures required by AASB 124 and AASB 1060.

KMP are those persons having authority and responsibility for planning, directing and controlling the activities of the entity, directly or indirectly, including any director. Remuneration disclosures include defining compensation for these KMP in aggregate (AASB 1060) or by category (AASB 124):

- short-term employee benefits e.g. cash salary and wages, paid leave, bonuses and non-monetary benefits.

- post-employment benefits i.e. amounts payable after the completion of employment (other than termination benefits below).

- other long-term benefits e.g. long service leave.

- termination benefits e.g. redundancy payments.

- share-based payments.

Further information is available:

- The Australian Charities and Not-for-profits Commission Amendment (2021 Measures No. 3) Regulations 2021

- The ACNC website: Financial and other reporting | Australian Charities and Not-for-profits Commission (acnc.gov.au)

- Your Prosperity Adviser.