Over the past few years, medical practices have come under increased scrutiny by state revenue offices as state governments seeks to shut down the perceived loophole allowing medical centre operators to avoid payroll tax obligations for the practitioners operating from those centres.

The decision from The Optical Superstore case in 2019 (VIC) set off the precedent for successive east-coast state governments in subjecting medical centre operators to payroll tax for the payments made to practitioners, with some operators facing backdated payroll tax liabilities and penalties ranging in the millions of dollars. This issue has been taken further resulting from the dismissal of the appeal of the Thomas and Naaz 2021 case (NSW) which upheld that payments collected on behalf of doctors and remitted were subject to payroll tax under the contractor provisions, as the payments to the doctors were for or in relation to the performance of their work for the medical centre.

Most recently, the Queensland government has seized upon the result of the Thomas and Naaz case and published a public ruling (PTAQ00.6.1) which outlined the Commissioner of State Revenue’s view that amongst other points, contracts between medical centres and practitioners are subject to payroll tax, regardless of the manner in which payment was collected and remitted, unless the practitioner or services falls within three very specific exemption categories.

While the public ruling is only the current view of the Commissioner that may be overridden by a later court decision to the contrary, and only directly applicable to Queensland employers, it is clear the Queensland government intends to target medical centre operators to close its tax revenue gaps. We have no doubt this view will soon spread to other eastern states and other Australian states and territories, so all medical centre operators should be on notice!

Examples of at-risk arrangements that may now run afoul of the payroll tax rules includes:

- Medical centre operators that collect patient billing and Medicare rebates on behalf of doctors into a practice trust account and remit the net amount after deducting agreed service fees >>> The ruling clarifies and expands upon the Thomas and Naaz case to clarify that it’s the nature of the ‘relevant contract’ that results in payments being subject to payroll tax under the contractor provision. Therefore the source and method of payment does not change whether a payment is subject to payroll tax.

- A contract between a medical centre and a practitioner may state the practitioner is the principal, and/or the medical centre only provides administrative services to the practitioner, such that the practicing doctor is not performing services for or on behalf of the centre’s patients >>> The ruling makes it clear that the Commissioner’s view is that such clauses do not prevent the application of the relevant contract provisions if the medical centre is able to “exercise operational or administrative control over the services provided to patients or is able to exercise operational or administrative control over a practitioner to influence decisions about who practises at the centre, when they practise, and the space within the centre where that occurs”. This is a significant change to the understanding up to now and significantly increases the scope of payroll tax application to medical centre operators.

What’s more concerning to the medical industry from this public ruling is that the ruling specifically states the term ‘medical centre’ is intended to incorporate all forms of health centres that engages practitioners of all types of medical services. This includes dental, physiotherapy, radiology, and other health services that the centre provides to the public via one or more licenced practitioners that is engaged as an independent contractor to the centre.

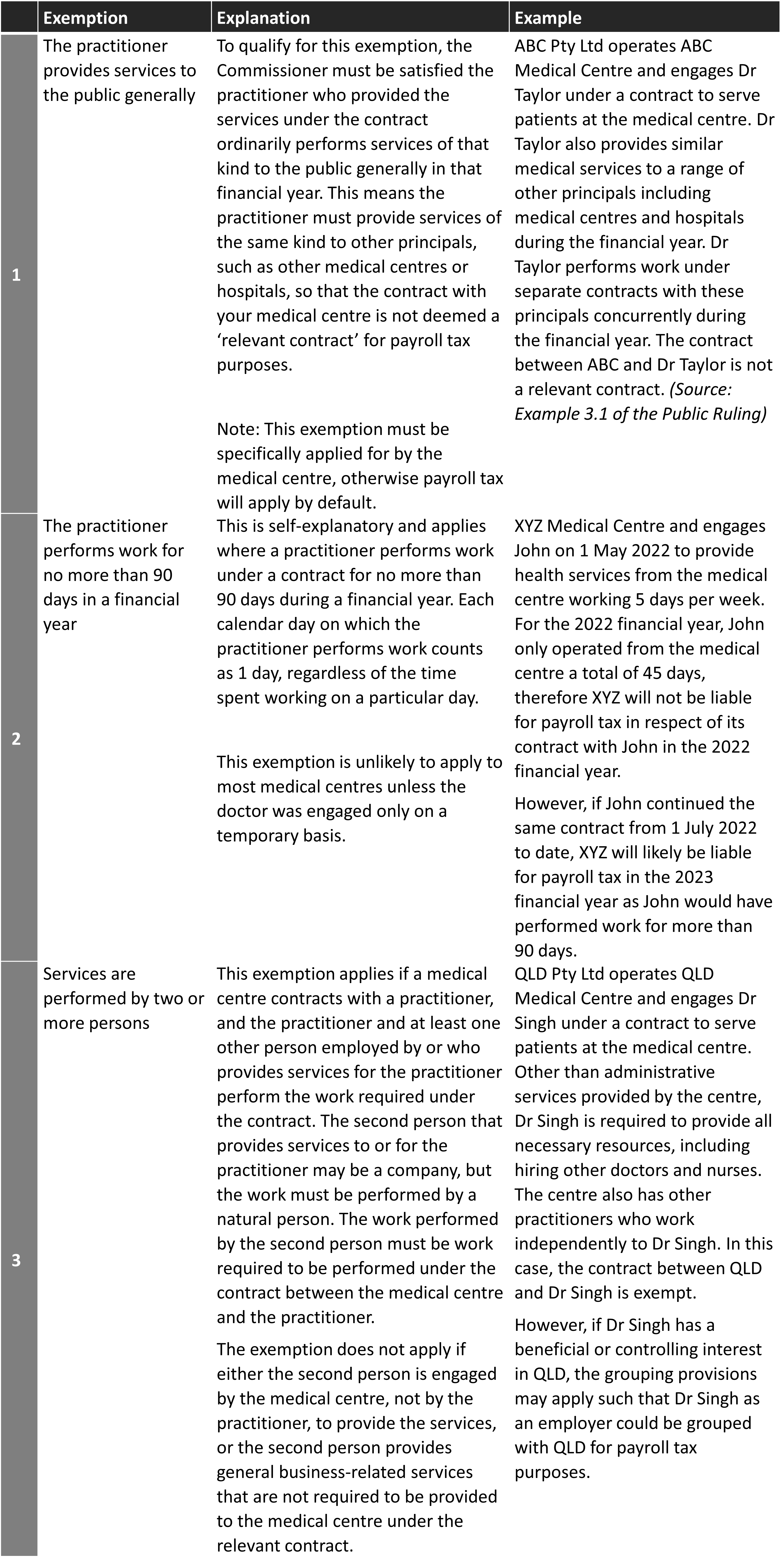

Does your arrangement qualify for one of the exemptions?

There are a number of exemptions from payroll tax under the legislation, and the Qld public ruling specifically highlights three of those that are more likely to apply to a contract between a medical centre and a practitioner.

We explain what each of these exemption means, and an example of how the exemption can apply.

Does this affect me?

If you operate a medical centre, particularly in Queensland, this will definitely affect you and you must take urgent action to review your tax exposure and get advice on the documentation of the contracts and arrangements your medical centre has with the practitioners.

One piece of good news from the recent developments is the Queensland government has publicly stated to the industry bodies (AMA, RACGP, amongst others) their commitment that they will not backdate payroll tax audits beyond the 2022 financial year. However, that still leaves open the tax risks on the 2022 and current financial years to affected Queensland practices. Further, there are no guarantees other states will adopt the same limited audit period, meaning for example a Victorian medical centre is still at risk of 5 or more years of payroll tax audits stemming from this issue.

Is this the end of agency agreements?

It has been common industry practice for medical centres to collecting patient billings on behalf of their contracting practitioners, with an agency agreement for the centre to forward the collections, net of agreed service fees, to the practitioner. However with the ruling, there is significant risk such arrangements will now be caught in the payroll tax net.

Could the answer to this problem be that the contracting practitioners need to reconcile their own billings versus centre operators having to pass on the additional payroll tax costs? Are there now technologies available to sufficiently reduce administrative time required by practitioners to do so?

If as a result of the recent developments you believe your medical practice may become at risk of payroll tax liabilities, and you believe any of these exemptions can apply to you, it is important to take immediate action to ensure your business contracts and arrangements can stand up to scrutiny. Alternatively, it may present an opportunity for you to review your current contracts and arrangements with a view of amending or changing the practice so that one or more of your contracting practitioners can fall within the exemptions available. Commercial realities and strategies should always be at the forefront to ensure the right decisions are made by your business.

What action should I take?

As with everything tax and business related, good documentation and proper timely professional advice is the key in ensuring you are managing and minimising adverse risks to your business.

- Proper contracts and documentation will ensure centre operators that provides administrative services or facilities only are not inadvertently caught by payroll tax;

- Consider the possibility of the application of any of the exemptions to your business;

- Ensure all current and future payroll tax obligations are adequately accounted for in your business plans and budgets;

- Review your business’ strategic decision around the business and commerciality;

- Above all, early engagement and planning is the best way to guarantee readiness to respond to any new tax risks faced by a business.

Make sure that your business can withstand a payroll tax review. Our tax experts are experienced in advising businesses in the medical industry and are happy to have an initial call to discuss any concerns you may have.

If you have any questions regarding the above, contact Director of Business Services and Taxation Brendan Campbell at bcampbell@prosperity.com.au or Manager of Taxation, Charles Yuan at cyuan@prosperity.com.au. Alternatively, we have Specialist Health Sector Advisers in each of our offices. If you would like to speak to one in your location, call 1300 795 515.